«Government bond» may be the most reassuring phrase in finance, and one of the most misunderstood. You lend money to a state; it pays you interest and returns your capital at maturity. Simple. But behind that simplicity are different names in every country, metrics few people really read, and one detail that changes everything: the yield is not the coupon. This guide lines it all up — from the basics to the numbers that matter — and shows how we compute them, from official sources.

Over 4,000 government bonds from more than 30 countries, from the official European register. Search yours and get real yield, duration and — for inflation-linked ones — the coupons computed to the cent from the ministries’ official coefficients. Updated every week: a living archive, not a list to browse.

Explore European government bonds →What bonds are (in plain words)

A bond is a loan. When you buy a government bond, you lend money to the state: in return you receive periodic interest — the coupon — and, at maturity, the repayment of the face value (usually 100 for every 100 lent). Four building blocks, always the same:

- Face value: the amount repaid at maturity (base 100).

- Coupon: the interest, as a percent of face value, usually paid every six or twelve months.

- Maturity: the date the capital comes back.

- Price: what you pay today on the market, which is not necessarily 100.

And price is exactly the confusing part. A bond can trade above par (over 100) or below par (under 100): buy at 98 a bond that repays 100 at maturity, and those extra 2 are part of your gain. That’s why the yield does not equal the coupon. The «clean» price you see quoted is the clean price; what you actually pay includes the interest accrued since the last coupon (the accrued interest). Every technical term is explained, one by one, in our bond glossary.

What they’re called in Europe (and why the name matters less than the type)

Every national Treasury gives its bonds its own names — BTP, Bund, OAT, Bonos — but behind the acronyms there are only a few recurring types: fixed coupon, zero-coupon (no coupon, bought below 100 and redeemed at 100), floating rate (the coupon follows market rates) and inflation-linked (capital and coupon revalue with the cost of living). Understanding the type matters more than remembering the acronym.

| Country | Main names | What they are |

|---|---|---|

| Italy | BOT · BTP · BTP€i · BTP Italia · CCTeu | Short zero-coupon, fixed coupon, inflation-linked (euro-area and Italy), floating rate |

| Germany | Schatz · Bobl · Bund · Bund€i | Fixed coupon at rising maturities (2 / 5 / 10+ years) and an inflation-linked version |

| France | BTF · OAT · OAT€i · OATi | Short zero-coupon, fixed coupon, inflation-linked (euro-area and France) |

| Spain | Letras · Bonos · Obligaciones | Short zero-coupon, medium and long-term fixed coupon, with the «indexadas» versions |

| Others | OT (Portugal) · DSL (Netherlands) · OLO (Belgium) · RAGB (Austria) | Same logic, different names: fixed coupon and inflation-linked versions |

The type isn’t a collector’s detail: it determines how the yield is calculated. A fixed bond is pure arithmetic; an inflation-linked one depends on an official coefficient that changes every day; a floater depends on future rates, which nobody knows in advance. You can browse each country’s live bonds in the Government bonds pages.

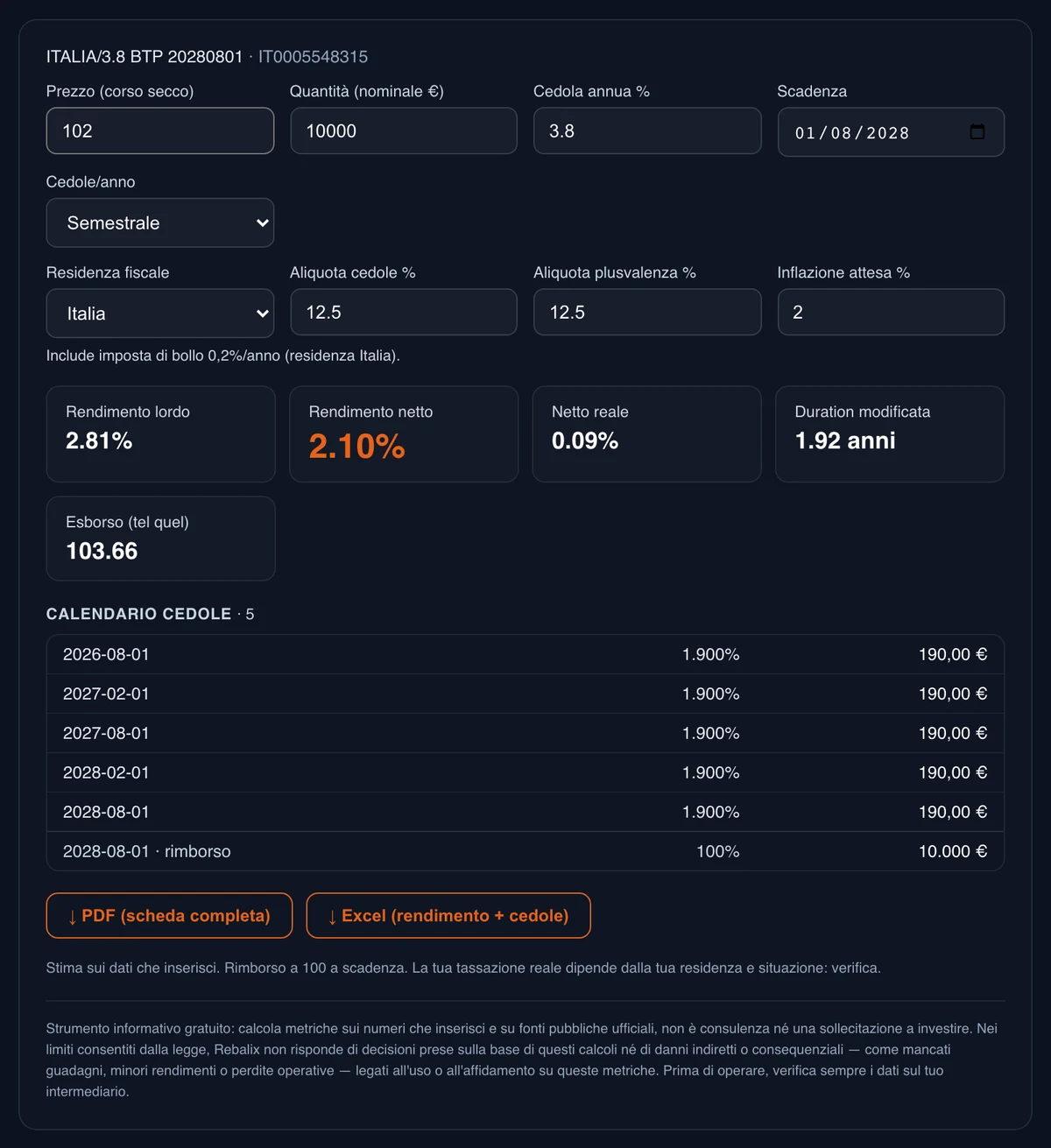

The metrics that matter — and how we compute them

The coupon tells you how much the bond pays out, not how much it returns to you. What really counts is a small dashboard of numbers:

- Gross yield to maturity: the rate that equates the price you pay today with all future cash flows (coupons + repayment), accounting for buying above or below par. It’s the real «how much it returns».

- Net yield: after the tax of your fiscal residence (in Italy the reduced 12.5% on government bonds) and stamp duty.

- Real yield: after expected inflation. It’s what matters for purchasing power — 3% nominal with 2% inflation is about 1% real.

- Modified duration: how much the price moves if rates change by 1%. It’s the measure of interest-rate risk.

- Accrued interest: the interest built up since the last coupon, on the international ICMA Actual/Actual convention. It’s the gap between the clean price and what you actually pay.

How we get them: a dated-cash-flow engine computes the yield as an annually compounded internal rate of return on the real flows, on the Actual/Actual convention; the net applies your residence’s rates (verified for Italy, France and Germany) plus stamp duty; the real uses the inflation you choose. The method, step by step, is on the Methodology page; you can try it on any bond in the calculator.

Not a list: a living archive

Many sources — even major ones — give you a list: ISIN, name, nominal coupon. Great for finding a bond, useless for knowing what an inflation-linked bond really yields, or what a coupon that revalues every day is worth. The difference isn’t the list: it’s the constant archival work behind it. To produce a correct figure we keep, updated over time:

- the official European register (source FIRDS / ESMA): over 4,000 bonds from more than 30 countries, updated every week;

- the inflation series (euro-area HICP, Italian FOI, the French index) from Eurostat and Istat;

- the official ECB exchange rates, for bonds denominated in a currency other than the euro;

- the indexation coefficients published by the debt agencies — MEF, Agence France Trésor, Finanzagentur, Tesoro Público — refreshed every month.

And a rule lists don’t have: when the official figure isn’t there, we don’t make it up. An inflation-linked coupon whose official coefficient is missing shows only the date, never an estimated amount. Better an honest blank than a wrong number passed off as certain. This is what makes our data computable, not just browsable — and the hardest case proves it best of all.

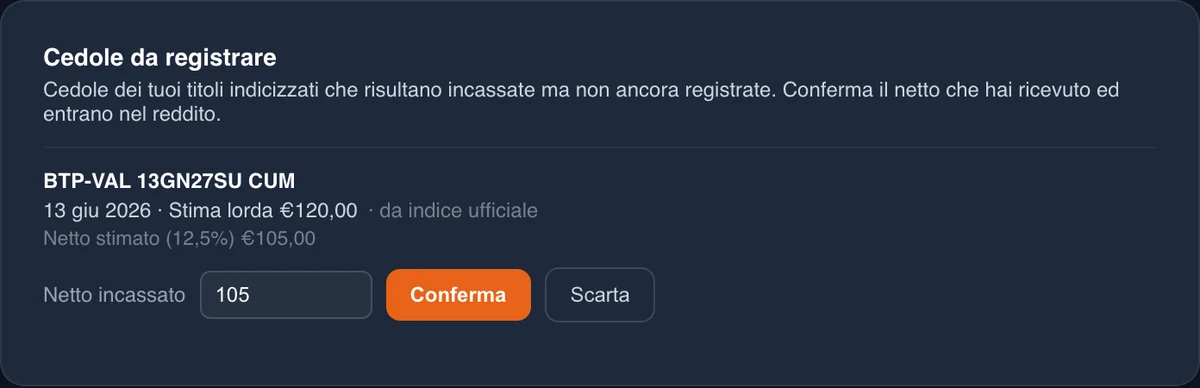

Inflation-linked coupons: the hardest case, computed to the cent

Of all bonds, inflation-linked ones are the trickiest to track. A plain bond has fixed coupons: 3% on €1,000 is €30 a year, done. A linker doesn’t: its coupon is revalued every day. The coupon that lands in your account is real rate × coefficient-of-the-day, and that coefficient appears nowhere on your statement. Redoing it by hand, for every payment, is impractical — so most apps either skip it or estimate it roughly.

We don’t estimate. We take the official indexation coefficient published by the debt agency and compute the coupon with the same convention they use: the international ICMA Actual/Actual standard, which also handles the «short» and «long» first coupons correctly. The result matches to the cent what you actually received. We cover 41 bonds, five families, two indices — euro-area inflation and, for French OATi, French inflation.

| Family | Country | Index tracked | Official source |

|---|---|---|---|

| BTP€i | Italy | Euro-area inflation | MEF |

| OAT€i | France | Euro-area inflation | Agence France Trésor |

| Bund€i | Germany | Euro-area inflation | Finanzagentur |

| Inflation-linked Obligaciones | Spain | Euro-area inflation | Tesoro Público |

| OATi | France | French inflation | Agence France Trésor |

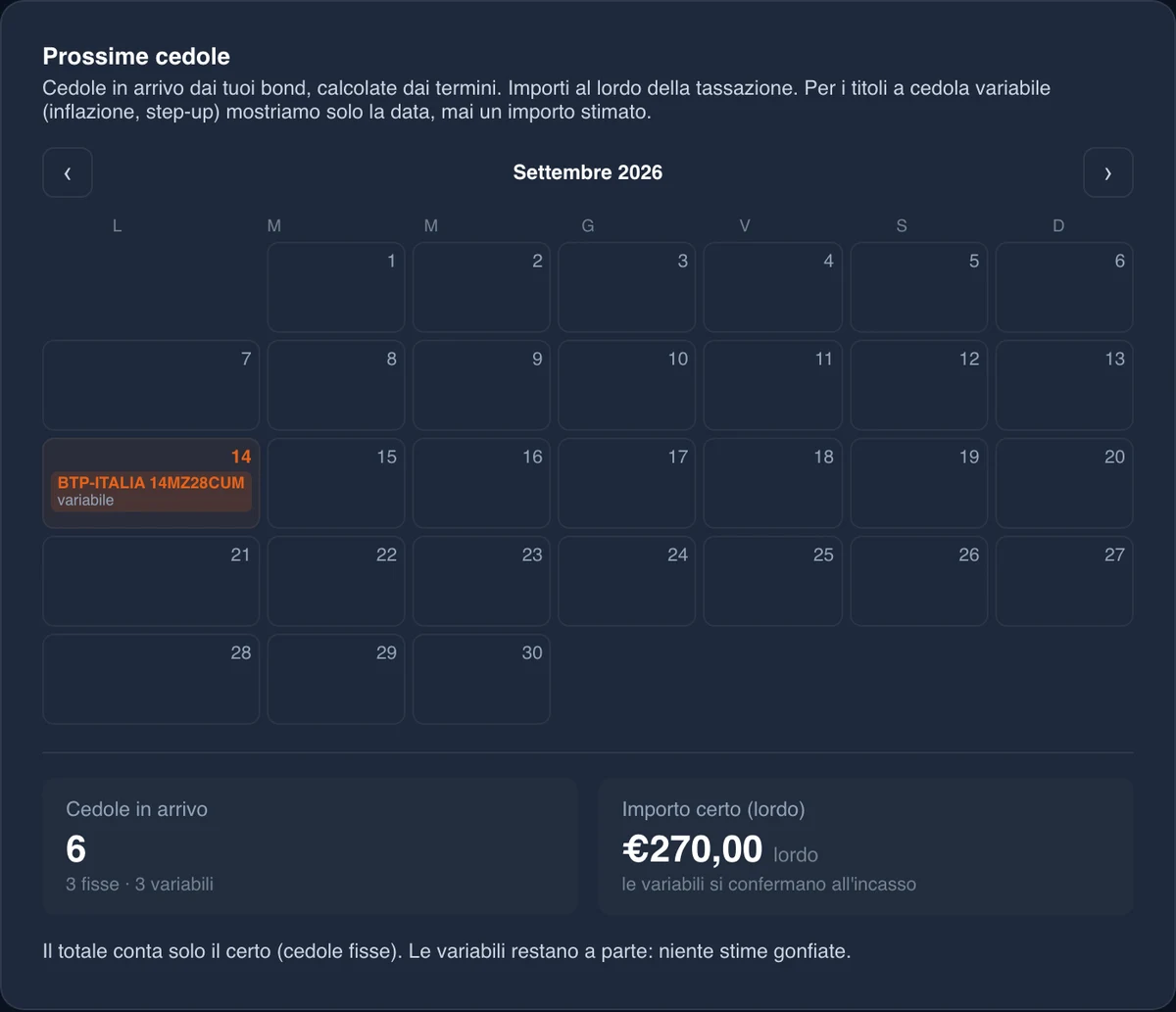

How they fit your portfolio

A government bond doesn’t live alone: it’s a line in your portfolio, next to ETFs, stocks and other bonds. Rebalix treats it that way — coupons become an income calendar, they feed your real return and add up with the rest, instead of staying an isolated number on a statement.

A method detail we’re often asked about: you enter the price you bought at, and update it whenever you like. It isn’t a limitation, it’s a choice. Yield depends on price, and we record what is yours — without turning into a terminal that nudges you to trade. Rebalix tells your portfolio’s past; it doesn’t push you to buy.

Diversify: issuer, duration, and mind the rating

Putting everything on a single bond, from a single country, with a single maturity is the opposite of prudence. There are three axes worth knowing — not as rules, but as maps to understand risk.

By issuer

Different countries carry different risk: the famous spread. Spreading bonds across several issuers reduces your dependence on the health of a single state.

By duration

Different maturities react differently to rate moves (that’s duration): the longer the maturity, the more the price swings. Staggering maturities — a «ladder» of bonds — spreads out interest-rate risk and the timing of when you reinvest.

The rating

The rating is the judgement of the main agencies (Moody’s, S&P, Fitch) on an issuer’s ability to repay its debt: a scale from investment grade (high quality) to high yield (more risk, more return demanded). It isn’t a guarantee and it’s an opinion that changes over time, but it’s a good starting point for weighing issuer risk.